McDonald’s SWOT Analysis (2026): Beyond the Burger

Written by Nicholas • Reviewed by Reginald, our mentor guide

⏱️ Read Time: 7-9 minutes

📅 Published July 18, 2025 • Updated June 28, 2026

TL;DR

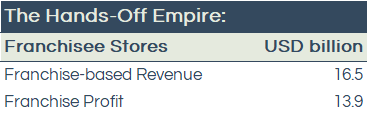

Franchise Machine: McDonald's keeps overheads low because ~96% of its restaurants are franchised.

Real Estate Moat: It isn’t just a burger business — it’s a landlord. It often owns or controls the land and buildings under its franchised stores, earning steady rent alongside royalties.

Strategic Snapshot: A SWOT analysis reveals unmatched scale but it needs to move faster on digital growth (opportunity) and respond to health-focused competitors (threat).

Sources used: This case study is based mainly on McDonald’s Form 10-K, Restaurants by Market 2024, Restaurants by Market 2025, and Franchise Disclosure Document Summary and competitor company materials from Yum Brands’ Q4 2025 Financial Summary (for KFC) and Restaurant Brands International’s Global Store Count (for Burger King).

Date last checked: June 2026. Figures are based on FY2025 company filings, investor materials and publicly available industry sources, which were the latest full-year materials available at the time of writing.

McDonald’s is not just a burger business.

It earns money through company-operated restaurants, franchised restaurants, brand strength and a business model shaped by scale and real estate-like economics.

The goal is not to decide whether to buy the stock — it is to learn how a business works.

McDonald’s SWOT Analysis at a Glance

Before we look at how McDonald’s makes money, here is the quick SWOT view:

Strengths: Brand, franchise network, scale, real estate, global presence, technology

Weaknesses: Labor challenges, menu complexity, franchisee dependence

Opportunities: International expansion, digital transformation and AI, healthier options

Threats: QSR competition, negative health perception, inflation and value pressure, PR controversies

We’ll unpack these later, after first understanding the business model behind the Golden Arches.

The Golden Arches Under the Monocle

Welcome back to Young Investor Journey! Our first step in analyzing any company is to understand what it is and how it actually makes money. For a giant like McDonald’s — a company we all think we know — there’s a surprisingly complex engine working behind the scenes.

The company’s investor relations page is a treasure trove of annual reports, quarterly updates and fact sheets. With the help of the powerful combination of AI assistance to process the data and our human mentor, Reginald, to guide and challenge us, I’ve dug in to answer the big questions.

First — What is McDonald’s?

We’ve all been there: you walk in, place your order and get your food in record time. McDonald’s didn’t just join the fast-food world; it pioneered the Quick Service Restaurant (QSR) model as we know it today.

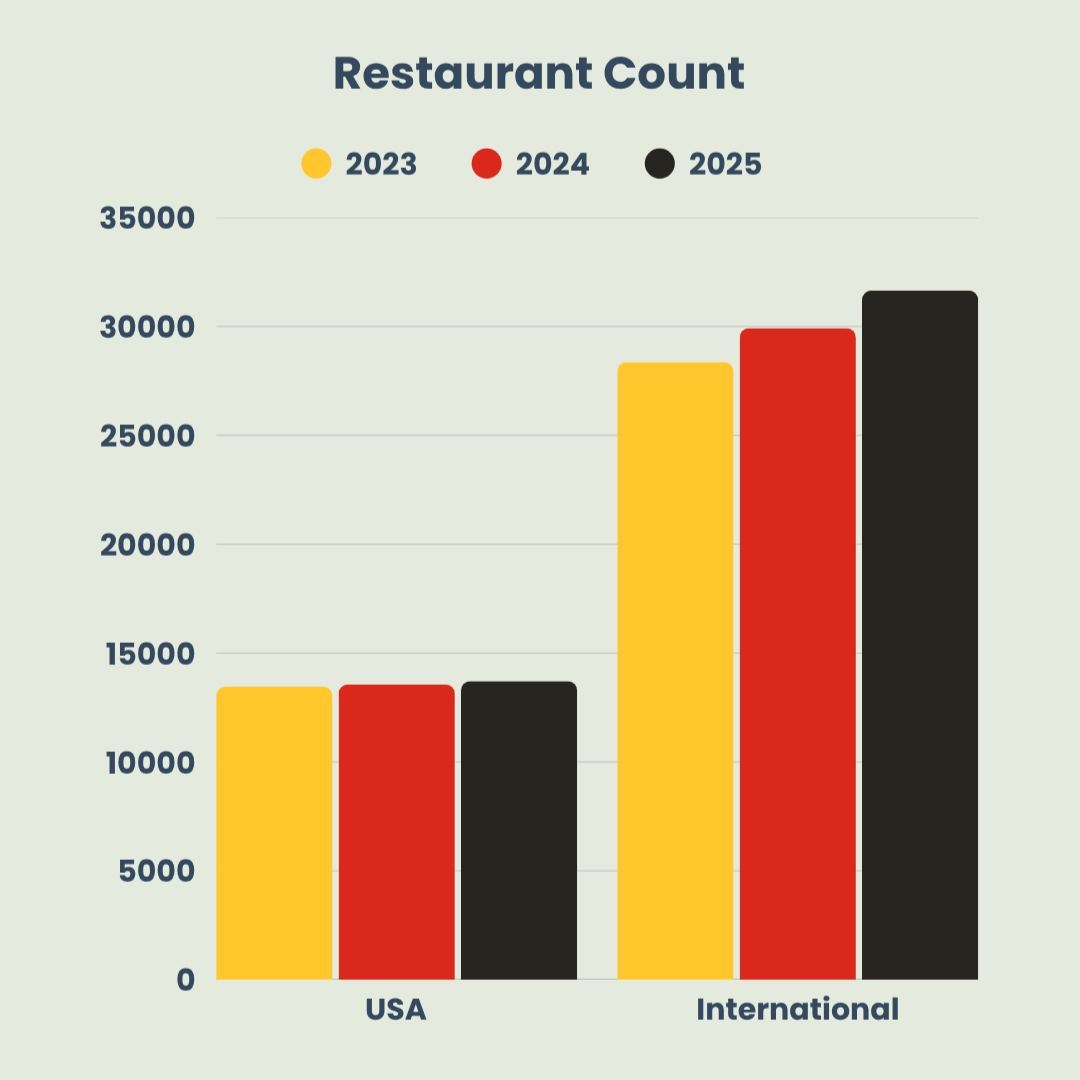

An American icon with a history spanning over 85 years, its Golden Arches are instantly recognizable worldwide. It isn’t just a logo; it’s a statement of global market leadership. As of the end of 2025, McDonald’s is the largest QSR chain on the planet, with an incredible 45,356 restaurants.

Second — How McDonald’s Actually Makes Its Money

This is where it gets interesting for us as investors. McDonald’s has two very different, but related, headline numbers: Corporate Revenue and Systemwide Sales.

In 2025, McDonald’s Corporate Revenue was $26.9 billion. This is the money the company actually records as sales and is generated in two main ways:

Company-Operated Restaurants:

McDonald’s directly operates a small fraction of its stores (~4%). These brought in $9.7 billion in 2025. This is the most obvious revenue stream — they sell burgers and fries and they keep the sales revenue. After paying for expenses of operating the stores, this generated $1.4 billion in restaurant profit.

Franchised Restaurants:

Here lies the true engine of the business. A staggering 96% of McDonald’s restaurants are run by franchisees. This model is brilliant because it provides steady, high-margin income streams.

Royalties and Fees: Franchisees pay an initial fee of $45,000 per restaurant and ongoing royalties, which are approximately 4-5% of their sales, to use the brand and system. This provides McDonald’s with a very profitable, low-overhead income.

Real Estate Empire: This is the secret sauce. McDonald’s often owns or controls the land and buildings for its conventional franchised restaurants. These sites are then leased out to franchisees who pay rent regardless of sales performance. This generates a significant and stable source of rental income. Furthermore, McDonald’s has first dibs on prime locations.

McDonald’s Secret Sauce: A Real Estate Empire?

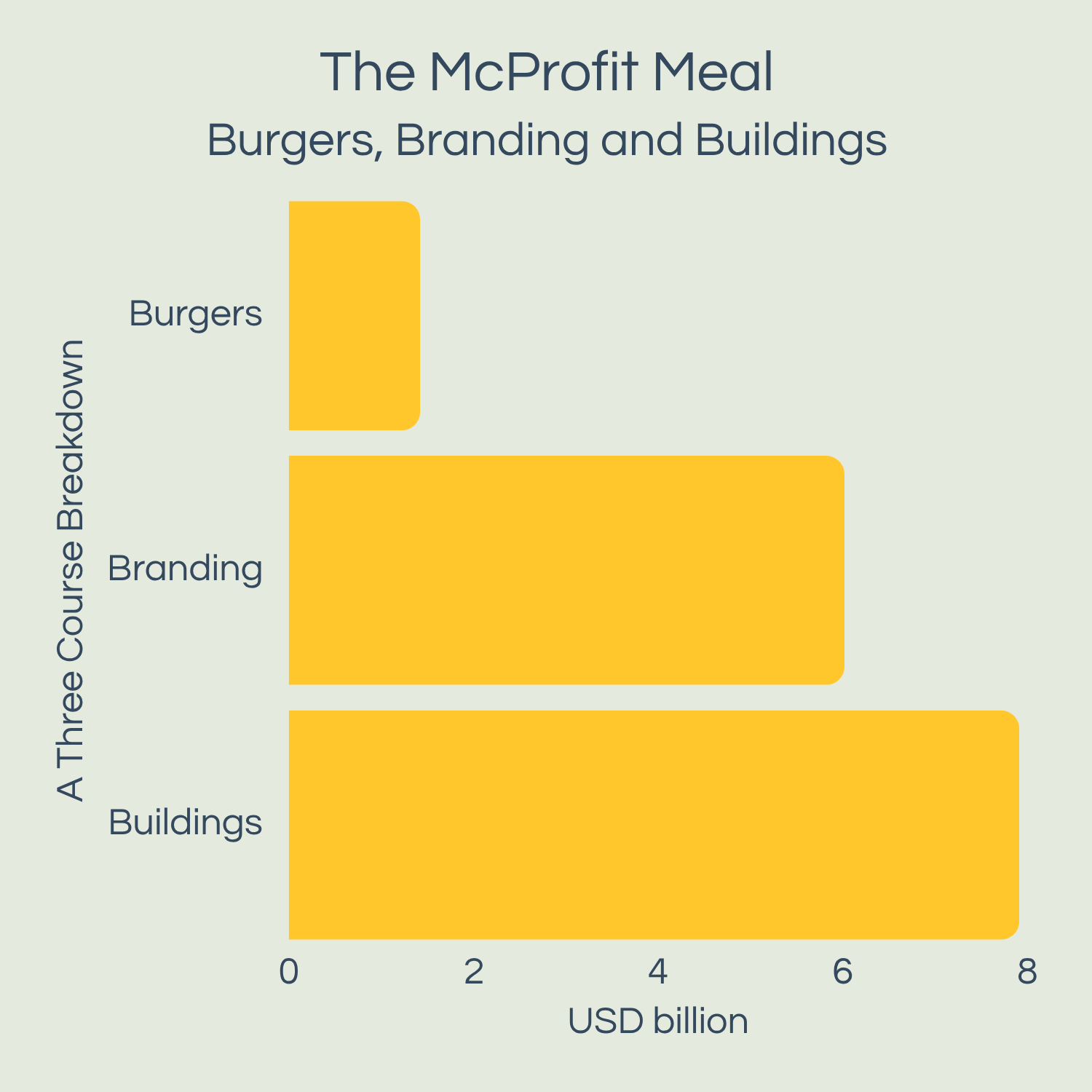

From these franchise-based streams, McDonald’s received $16.5 billion in 2025. As the associated costs are so low, this generated a massive $13.9 billion in profit. This is where the secret sauce is revealed. The real business isn’t selling burgers, it’s being a landlord. The majority ($7.9 billion) of that staggering profit comes from rent. To see how this really works, we can break down their entire profit model into a simple framework I call “Burgers, Branding and Buildings.”

Burgers: The profit from the restaurants they run themselves.

Branding: The high-margin profit from royalties and fees.

Buildings: The stable, powerful profit from real estate rent.

So, what about the huge numbers you see in the news? That’s systemwide sales. This is the total sales generated by all McDonald’s restaurants, both company-operated and franchised.

In 2025, this figure was a mind-boggling $139.4 billion.

To put that in perspective, while systemwide sales are not the same as GDP, the figure is larger than the annual GDP of many countries, like Ecuador, Dominican Republic and Oman!

Source: McDonald’s FY2025 Form 10-K for systemwide sales; IMF World Economic Outlook Database, April 2026 edition, for selected country GDP. Used as a rough scale comparison only.

SWOT Analysis: A Deeper Look

Now that we understand the business model, let’s evaluate the company. A SWOT analysis is the perfect tool to map out its internal Strengths and Weaknesses against its external Opportunities and Threats.

McDonald’s Strengths

Iconic Brand Value: From the Golden Arches to the “i’m lovin’ it” slogan, McDonald’s is a cultural phenomenon. This brand power translates to strong customer loyalty and a dominant market position.

Powerful Franchise Network: With over 45,356 restaurants at the end of 2025, McDonald’s dwarfs its competition (Burger King has 19,900 stores and KFC has 33,897). This massive scale provides a large, reliable base of royalty payments and creates immense purchasing power, driving down costs.

Real Estate Portfolio: Owning the majority of its restaurant buildings provides a stable, high-margin income from rent, insulating the company from the daily volatility of the fast-food business.

Unmatched Global Presence: With 69% of its restaurants operated outside the US and in over 100 countries, McDonald’s successfully blends its core menu (Big Mac and Happy Meals) with local favorites (like the McSpicy here in Singapore!), demonstrating a unique ability to adapt to diverse tastes.

Embracing Technology: From self-service kiosks and McDelivery to the MyMcDonald’s Rewards loyalty program, the company invests heavily in technology to improve customer experience. Those loyalty points are a clever way to promote treats — it’s certainly my favorite way to cash in for a McFlurry!

Investor lens: Are McDonald’s brand, scale and real estate advantages still getting stronger, or are competitors slowly catching up?

McDonald’s Weaknesses

Labor Challenges: Like much of the QSR industry, McDonald’s faces high employee turnover, often linked to less competitive wages and poor work perception. This can impact service consistency and operational efficiency, although this is partly mitigated by a simplified and standardized workflow.

Menu Complexity: A vast and sometimes bloated menu can overwhelm customers and complicate kitchen operations, potentially slowing down that “quick service” promise.

Franchisee Dependence: McDonald’s powerful franchise model also means it depends on franchisees to run restaurants well, manage costs and protect the customer experience. If franchisees come under pressure, the wider McDonald’s system can feel the strain too.

Investor lens: Which weaknesses are temporary problems and which ones could weaken the business model over time?

McDonald’s Opportunities

Expansion in Developing Markets: While already a giant with 31,650 stores overseas, McDonald’s still has room to grow in underpenetrated and rapidly developing economies. Between 2023 and 2025, the company has seen a 3,285 outlet increase overseas.

Digital Transformation: The company continues to invest heavily in technology, with a focus on integrating AI and digital platforms to personalize the customer experience, drive loyalty and streamline operations.

Healthier Options: As global tastes shift towards healthier eating, McDonald’s can capture a wider audience by expanding its health-conscious choices, such as its sub-500 calories options, plant-based meals or healthier drink options.

McPlant With Beyond Meat: A Healthier Option

Investor lens: Are these opportunities big enough to move the needle for a company as large as McDonald’s?

McDonald’s Threats

Intense Competition: The QSR market is saturated. McDonald’s faces constant pressure from traditional burger rivals like Burger King and alternatives like Subway and KFC, all fighting for the same customers.

Negative Health Perception: The global trend towards healthier eating is a significant long-term challenge. The association of fast-food with health problems, such as diabetes and obesity, is a persistent threat to the brand’s image.

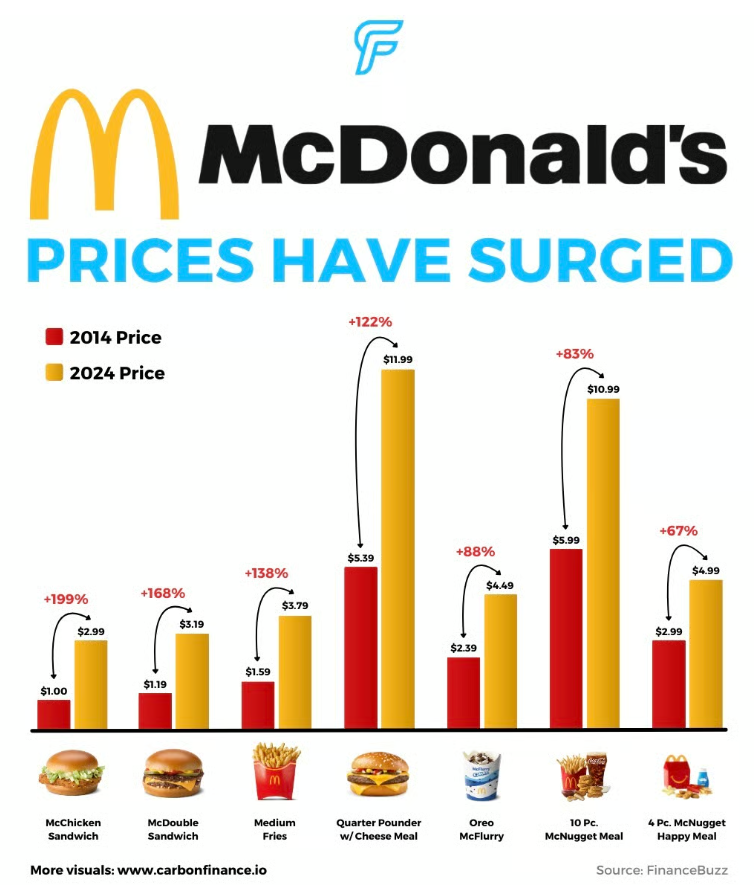

Economic Factors: Rising ingredient and labor costs have led to higher menu prices, with a popular FinanceBuzz study highlighting that McDonald’s prices for popular menu items rose by over 100% from 2014 to 2024. If customers start to see McDonald’s as less affordable, it could weaken one of the brand’s key historical advantages: value for money.

Visual: Carbon Finance; Data: FinanceBuzz, “Is Fast Food Affordable Anymore? Here’s How Menu Prices Have Changed Over the Years”

Ethical and PR Controversies: As a global brand, McDonald’s is under constant scrutiny. Controversies, such as the boycotts related to the conflict in Gaza, can quickly impact regional sales and damage brand perception.

Investor lens: Which threats could actually damage McDonald’s moat and which are just normal business challenges?

McCafé SWOT Analysis: A Mini Example

McCafé is not a separate business from McDonald’s, but it is a useful mini-example within the wider SWOT analysis.

Strength: McCafé gives McDonald’s another way to compete for everyday customer visits, especially in breakfast and coffee occasions.

Weakness: It still sits inside the McDonald’s brand, which means some customers may not see it the same way they see dedicated coffee chains.

Opportunity: Coffee is a repeat-purchase category and McCafé can support digital orders, loyalty rewards and higher-frequency visits.

Threat: Dedicated coffee chains, convenience stores and local cafés all compete for the same customer habit.

In simple terms, McCafé shows how one product category can support McDonald’s wider strategy, but it also faces its own competitive pressures.

Conclusion

This analysis gives us a solid framework. We see a powerful, resilient company with a brilliant business model, but one that is not without its challenges.

This context is crucial as we move forward. In our next case study post, we’ll use Porter’s Five Forces to dive deeper into the competitive landscape McDonald’s navigates.

To make sure you don’t miss it, subscribe to our newsletter and get the next post delivered straight to your inbox!

Going Straight to the Source

As Reginald always reminds us, the first step in any analysis is getting good data. For this deep dive, we pulled all financial data and restaurant counts directly from official sources and company materials, plus a franchise disclosure summary for franchise fee and royalty information: McDonald’s Form 10-K, Restaurants by Market 2024, Restaurants by Market 2025 and Franchise Disclosure Document Summary, Yum Brands Q4 2025 Financial Summary (for KFC) and Restaurant Brands International Global Store Count (for Burger King). This is a crucial habit for any young investor and one we’ll stick to on our journey.

Let’s keep growing together 🌱

— Nicholas

Frequently Asked Questions

-

It's one of the best learning cases available — not necessarily because it's the right stock to buy, but because the business model is easy to understand from daily life, the financials are publicly available and well-documented and it has enough complexity (franchise model, real estate, global operations) to stretch your analytical thinking. That's exactly why we start here — McDonald's is the first company we study on Young Investor Journey and for good reason.

-

This post isn't a buy or sell recommendation — it's a breakdown of the business model so you can practice thinking like an investor. Whether McDonald's makes sense for your portfolio depends on your own goals, risk tolerance and research. What this post gives you is the foundation: understanding how the business actually makes money before you look at the price.

-

A franchise is an arrangement where an independent operator — the franchisee — pays for the right to run a business under an established brand. For McDonald's, this matters enormously: roughly 96% of its restaurants are franchised, meaning McDonald's collects royalties, fees and rent without bearing most of the day-to-day operating costs. It's a highly scalable model that generates reliable, high-margin income.

-

Largely, yes. McDonald's often owns or controls the land and buildings for its conventional franchised restaurants, then leases those sites to franchisees who pay rent regardless of how their sales are doing. In 2025, rental income contributed $7.9 billion of McDonald's franchise profit — more than royalties alone. It's one of the most underappreciated parts of the business model.

-

Yes. McCafe broadens McDonald's product mix beyond burgers and fries, adding coffee and beverages that drive additional purchase occasions — including standalone coffee runs that wouldn't otherwise bring someone to McDonald's. It also helps the company compete directly with Starbucks and local cafes in the premium coffee segment. For investors, it's worth noting as a revenue diversification play within the same store footprint, adding income without the cost of opening new locations.

-

Systemwide Sales is the total value of everything sold across all McDonald's restaurants globally — including franchisee-run stores. In 2025 that figure was $139.4 billion. Corporate Revenue is what McDonald's itself collects: sales from its own restaurants plus franchise fees, royalties and rent — which came to $26.9 billion. The gap exists because most restaurants are franchised, but that's by design. The franchise model is where the real power is — in 2025, the franchise segment generated $13.9 billion in profit on $16.5 billion in revenue. That's an extraordinarily high margin and exactly why McDonald's prefers this model.

-

SWOT stands for Strengths, Weaknesses, Opportunities and Threats. It keeps your analysis balanced by forcing you to look at both the good and the bad. For McDonald's, the SWOT revealed unmatched scale and a powerful real estate moat as key strengths — but also real threats from rising prices, health-conscious consumers and intense competition. Without a SWOT, it's easy to get swept up in the strengths and miss the risks entirely.

-

Follow the same flow used in this post: start by understanding how the business makes money, identify the key drivers behind that revenue, map out the key risks using a SWOT, then verify everything against official filings like the Annual Report or 10-K. Finally sanity-check your conclusions with trusted secondary sources. The framework works for any publicly listed company — and McDonald's is a good one to practice on first because the business model is easy to grasp from daily life.

Spotted an error?

Email us at contact@younginvestorjourney.com. We review factual corrections and update articles where needed.

Continue this Journey

Read this next: McDonald's Five Forces Analysis: The Battlefield Report

McDonald's Five Forces Analysis: The Battlefield Report

What is a Moat? A Beginner’s Guide

First Investment? Why I Chose McDonald's as My First Case Study

Watch on Instagram

Prefer the visual breakdown?

About Young Investor Journey

I’m Nicholas — a young investor learning out loud. With guidance from my mentor, Reginald, and illustrations by Timothy, we break down complex investing ideas into plain English — no fluff, no jargon, just clarity.

How We Think

We help you build a framework you can apply to any company. Our framework is simple: understand the business model first, confirm with official reports, then sanity-check with trusted sources. The goal is to teach you how to think — not what to buy.

Education Only: We are here to share what we learn, not to give financial advice. Always do your own research and consider your personal goals, risk tolerance and financial situation before investing.